Global Interiors Outlook: Growing Pains

In the first part of Aircraft Cabin Management’s Global Interiors Outlook, Gary Weissel and Jeff Luedeke of Tronos Aviation Consulting mull the impact of the return to open borders for the aircraft interiors industry in 2023.

Read the latest issue of Aircraft Cabin Management.

December marks the three-year anniversary since the first human cases of COVID-19 were identified in China. Some may argue we are still in the pandemic. However, borders began to open roughly a year ago, which has spurred a recovery in air travel.

With international travel beginning to open at the end of 2021, 2022 started with optimism that airline travel demand would follow, and interior product demands would resurge. We know from historical data that airlines typically will limit spending to essential needs, until operating profits are realised in consecutive quarters, and a near-term outlook indicating continued financial stability.

2022 Passenger Volumes at a Glance

IATA’s Quarterly Chartbook Q3 2022 indicates that global passenger traffic Origin-Destination (“O-D”) in March 2020 was tracking close to 50% of March 2019 volume. Global passenger traffic O-D continues to climb and by September 2022 was at 81% of the pre-pandemic level. The upward trends were expected to continue for the remainder of the year. However, recent concerns over a potential recession and skyrocketing inflation may have some impact on Q4 volume expectations. In late November, Bloomberg Intelligence’s analysis reported that both corporate and leisure bookings were down, ‘possibly signalling that consumers were responding to pressured budgets’.

IATA is predicting that regional passenger recovery will be fully realised in North America in 2023; Europe, Latin America & Caribbean, and the Middle East in 2024; followed by Africa and Asia Pacific in 2025. Net total overall regional passenger recovery in the World in 2024.

2022 Financial Performance at a Glance

The end of Q1 resulted in some airlines reaching profitability again, and this continued with strong travel in Q2 resulting in others reaching profitability as well. Some airlines are seeing record revenues in Q3 with profitability. A few of the more prevalent earnings reports are as follows:

- July 29, Singapore Airlines reported a net profit of $370M USD April-June, which is a recovery from a $409M USD loss in the same period a year ago.

- October 13, Delta Air Lines announced their September quarter 2022 profit indicating record quarterly revenue and second consecutive quarter of double-digit operating margin. It was noted that demand improvement in corporate and international travel contributed.

- October 20, American Airlines reports the third quarter load factors were 85.3%, quarterly revenue record of $13.5B USD, a 13% increase versus 2019. It was noted that demand for domestic and short haul international travel remained very strong, with expected demand improvement for long-haul international travel as travel restrictions and testing requirements are lifted around the globe.

- November 7, Ryanair posted its largest ever after-tax profit for the six months to September at 1.37 billion euros ($1.37 billion). However, noted that regional developments make the sector fragile for the coming winter.

2022 Passenger Volume and Financial Performance Summary

The optimism for airline travel and financial recovery was realised through Q3 with overall passenger traffic (O-D) at roughly 81% of 2019 levels, and total industry revenues expected to recover to 93% of 2019 levels. Some markets such as Asia Pacific are not recovering as quickly due in part to travel restrictions remaining in place longer than other markets.

2022 Commercial Aircraft Interior Market at a Glance

TAC and Real Response Media independently performed surveys with a handful of interior product suppliers to get an understanding of business recovery, supply chain issues, and staffing levels.

Interior product suppliers are reporting business has rebounded to 60-80% of 2019 volumes. Of the current reported business, 20-30% is new business, while the balance is effectively restarting of 2019 projects put on hold when the pandemic hit. Requests for Quotation for new business have steadily been increasing over the previous six months.

Supply chain issues remain relevant, mainly related to raw materials and microprocessors, with added pressures from rising energy costs and logistics. Suppliers have tried to manage these challenges with restructuring, investing in stock based on forecasting, and investments in tooling / capabilities allowing sourced items to be made in house providing greater controls. Most that we talked to believe we are through the worst of the supply chain challenges and slowly climbing out of the hole.

Staffing levels have recovered back to 60-80% of 2019 levels. Every supplier we contacted is looking for new staff members. The biggest challenge was stated in degree technical positions, such as engineering. However, continued difficulties in fulfilling entry level manufacturing positions are evident as well. Suppliers have either enhanced their efforts or developed partnerships in their local communities, as well as applicable universities, to help create and improve the supply of new staff members.

Aircraft Interiors Market Outlook

The Aircraft Interiors Market Outlook is driven by fleet sizes, cabin age, new product trends and new product introductions. TAC, in partnership with Aerodynamic Advisory, annually produces a 10-year interiors market forecast covering line and retrofit interiors production.

The 10-year fleet growth is forecast to include approximately 17,600 new deliveries. Including fleet retirements, this predicts a 2031 fleet size over 33,000 aircraft.

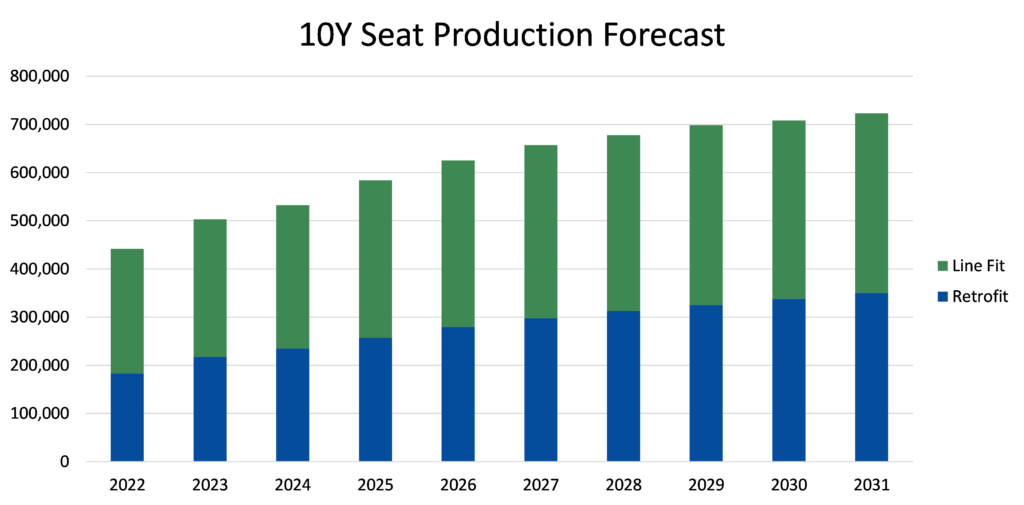

To support this projected fleet growth and fleet retrofits, TAC forecasts the need for 6.2 million new pax places, 2.8 million for retrofit of existing fleets and 3.4 million for new production line fit aircraft. This equates to approximately US$31 billion in seat production value. This is down about 25% from pre-pandemic forecasts over the same 10-year period, driven by reduced pandemic demand and slower fleet growth from pre-pandemic forecasts.

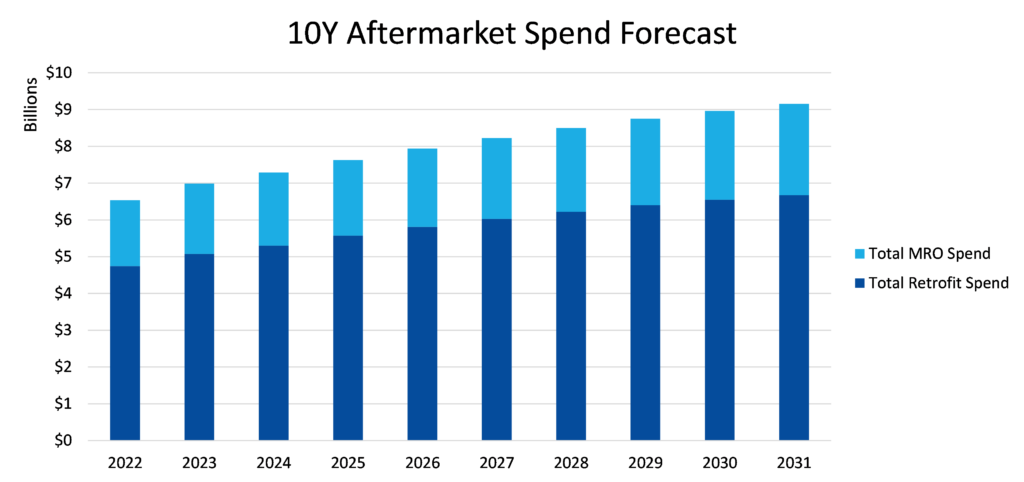

The total aftermarket spend on interiors is estimated at US$80 billion over the next 10 years. This is approximately US$22 billion in maintenance, repair and overhaul (MRO) of existing interiors and US$58 billion on installation of new replacement interiors – aka retrofit.

The total 10-year interiors production forecast in major product categories (including seats, galleys, bins, monuments, IFE, etc.) is forecast to be US$121 billion, split approximately 50/50 between retrofit and new line fit production. This is down about 12% from our pre-pandemic forecasts.

Aircraft Interior Market Trends

As much of the current business in the interiors supplier market consists of restarting programmes that were in the works pre-pandemic, there are limited areas of innovation evident. One of the results of the global lockdowns is more demand for Personal Electronic Device (PED) connectivity while airborne. Passengers feel the need to maintain connectivity while in the air to stay in touch with family, friends, social media and breaking news.

With connectivity there is a need to make charging available on board for PEDs. USB-C technology has continued to evolve in PEDs and will become the standard within the near future. A recent detailed assignment we performed indicated In-Seat Power Systems (ISPS) are playing catch up to a baseline USB-C with 60watt output capability. We anticipate technology advancements overall in ISPS as the system architecture and components are due for updates.

Business class cabins on international routes are still an area to monitor. With this market segment still trailing domestic demands, it may be too early to determine if the seat counts are sized appropriately for the post-pandemic demand. There has been plenty of speculation that reductions may be needed as virtual meetings became the norm during the lockdowns. However, we have recently seen the introduction of the ‘business plus’ first row, offering enhanced products and personal space. Several airlines have also announced the impending halt of international first class cabins as the level of business class services and seat offerings have closed the gap between the two classes.

The resurgence and continued growth in domestic and regional travel keeps the pressure on production volumes of narrowbody aircraft. Both Boeing and Airbus are still struggling with supply chain issues in their attempts to meet their own robust forecast production rates. The introduction of newly delivered narrowbody aircraft to increase existing fleets has spawned interior refresh demands on these existing fleets. We are seeing passenger seating replacements ahead of traditional trends, and the new oversized overhead stowage bins on the A320 airframe series, provides an opportunity to retrofit the existing fleets.

The airlines are once again making money, and travel demand is still evident, typically resulting in new business opportunities to come for suppliers.

Gary Weissel (managing officer) and Jeff Luedeke (managing director) Tronos Aviation Consulting, Inc. (TAC)