Jet fuel price impacting airline margin forecasts

Jet fuel prices remain approximately 54% above pre-conflict levels (as of 08 April), despite easing from a peak of $114 per barrel on 08 April, following a temporary ceasefire.

Analysis from IBA Insight reports that this sustained volatility is continuing to impact airline cost bases unevenly and drive secondary effects across fleet planning and aircraft asset values.

READ: Ceasefire brings fragile relief, but fuel crisis is far from over

In calculating the effect of higher fuel prices, IBA has considered the proportion of Cost per Available Seat Kilometre that fuel represents by region, hedging and localised effect on jet fuel cost.

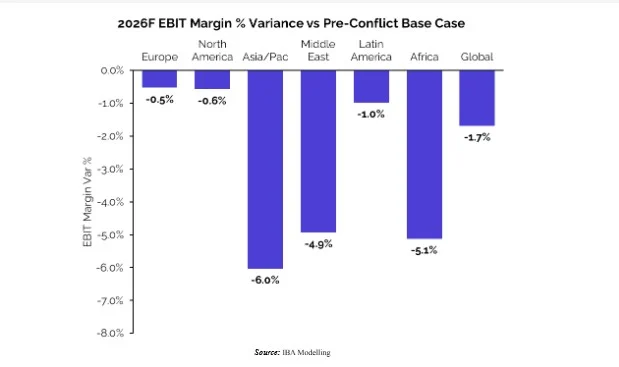

Based on the assumption that fuel prices remain elevated over the next 12 months, IBA has applied the following indicative modifiers to its regional Earnings Before Interest and Taxes (EBIT) margin forecasts:

IBA analysis suggests that elevated fuel prices could reduce airline profitability globally, with 2026 EBIT margins forecast to decline by 1.7 percentage points to 5.5% from pre-conflict base case assumptions of 7.2%. The analytics company expects that this impact is expected to vary significantly by airline per region, with those in Asia-Pacific likely experiencing the largest margin reduction. EBIT margins are forecast down by six percentage points, reflecting a higher proportion of long-haul operations, relatively lower fuel hedging coverage and exposure to competitive international markets.

It also highlights that airlines in the Middle East (-4.9 percentage points) show a similar trend, driven by fuel-intensive long-haul hub models, while Africa (-5.1 percentage points) reflects structural cost challenges, including older fleets, lower load factors and limited pricing power.

By contrast, the organisation anticipates more moderate impacts are forecast for airlines in North America (-0.6 percentage points) and Europe (-0.5 percentage points), due to hedging strategies, higher domestic market share, and stronger pricing power helping offset fuel cost pressures.

IBA’s analysis also shows that airlines in North America remain the least exposed to jet fuel price volatility, supported by domestic supply dynamics, with jet fuel prices broadly tracking 100–110% of last year’s levels.

Asia-Pacific and Middle Eastern airlines are the most exposed, with jet fuel costs rising by around 60%, while European and African airlines have seen increases of approximately 40%.

IBA notes that Europe continues to benefit from high levels of hedging jet fuel prices, with many major carriers more than 80% covered for 2026, although this protection is expected to unwind into 2027. It also warns that, despite recent price easing, ongoing fuel market volatility will continue to shape airline profitability, with wider implications for capacity, network planning and fleet strategy.